The Debate Burns On

Greg Mankiw challenges my interpretation of Arthur Burns’ legacy. Monetary policy, he points out, affects inflation with a lag. Once you take the lag into account, Burns looks quite bad, since the inflation rate fell a bit during the first year of his term (presumably due to his predecessor’s efforts) and rose dramatically during the year after he left.

At first, my quant hand was pretty much convinced by Greg’s argument. After all, when you run the numbers, it’s quite unambiguous: monetary policy variables have only a slight impact on contemporaneous inflation; most of the impact comes later. But my rational economist hand wasn’t so sure, and in the end, it managed to convince my quant hand that Burns was, as I had originally suggested, more a victim of his predecessor’s excesses than a contributor to runaway inflation.

To illustrate, let’s start with a comment from Greg’s post. Happyjuggler0 writes:

Fair enough, maybe Burns should have paid more attention to what Friedman said. But what I notice is that Friedman made his statements (beginning with his 1968 American Economic Association presidential address) long before Burns took office. If Friedman could already see, two years earlier, that the Fed was losing its credibility, how could that loss of credibility have been Burns’ fault? (That line of reasoning is actually what got me thinking about this question in the first place.)

What’s particularly puzzling is the rapidity with which inflation accelerated during the year after Burns left. The inflation rate rose by almost 3 percentage points within less than a year, and that was with the unemployment rate around 6%, hardly a level one would normally associate with a dramatically overheating economy. The data don’t offer me any obvious clues as to what’s going on, but I would suggest that the credibility of monetary policy under then-current chirman G. William Miller may have had more to do with the problem than excessive ease during Burns’ final year.

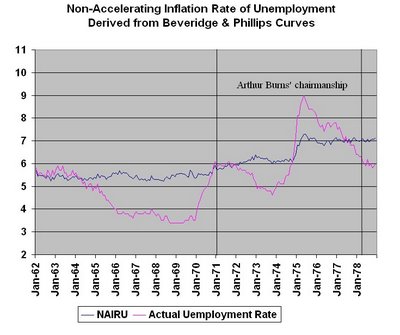

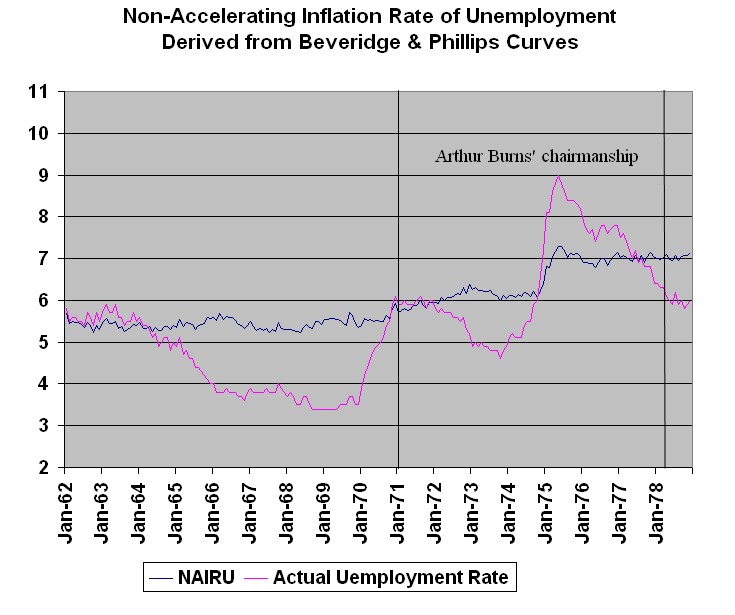

If we look at Burns’ overall period of chairmanship, it does not appear that he was, on average, pushing the economy beyond its limit. Consider this blowup of part of a chart that appeared in an earlier post. You can quarrel with my NAIRU methodology, but I don’t think the estimates are very far from the consensus. And what it shows is that, in terms of the employment gap, the weakness during the second half of Burns’ chairmanship roughly compensated for the strength during the first half, whereas during the years before Burns took over, there was a persistent period of inflationary high employment.

At first, my quant hand was pretty much convinced by Greg’s argument. After all, when you run the numbers, it’s quite unambiguous: monetary policy variables have only a slight impact on contemporaneous inflation; most of the impact comes later. But my rational economist hand wasn’t so sure, and in the end, it managed to convince my quant hand that Burns was, as I had originally suggested, more a victim of his predecessor’s excesses than a contributor to runaway inflation.

To illustrate, let’s start with a comment from Greg’s post. Happyjuggler0 writes:

All I'll say to that is that Milton Friedman publicly predicted the stagflation of the 70's before it happened, indeed before the word was even coined. It was a nonexistent phenomenon before then. It is not Dr. Friedman's fault that both Burns and the 70's presidents ignored him. It is not like Friedman was quiet about his views either....

Fair enough, maybe Burns should have paid more attention to what Friedman said. But what I notice is that Friedman made his statements (beginning with his 1968 American Economic Association presidential address) long before Burns took office. If Friedman could already see, two years earlier, that the Fed was losing its credibility, how could that loss of credibility have been Burns’ fault? (That line of reasoning is actually what got me thinking about this question in the first place.)

What’s particularly puzzling is the rapidity with which inflation accelerated during the year after Burns left. The inflation rate rose by almost 3 percentage points within less than a year, and that was with the unemployment rate around 6%, hardly a level one would normally associate with a dramatically overheating economy. The data don’t offer me any obvious clues as to what’s going on, but I would suggest that the credibility of monetary policy under then-current chirman G. William Miller may have had more to do with the problem than excessive ease during Burns’ final year.

If we look at Burns’ overall period of chairmanship, it does not appear that he was, on average, pushing the economy beyond its limit. Consider this blowup of part of a chart that appeared in an earlier post. You can quarrel with my NAIRU methodology, but I don’t think the estimates are very far from the consensus. And what it shows is that, in terms of the employment gap, the weakness during the second half of Burns’ chairmanship roughly compensated for the strength during the first half, whereas during the years before Burns took over, there was a persistent period of inflationary high employment.

The implications of this chart are quite specific, given the coefficients of my Phillips curve. If we assume a 6-month lag in the effect of monetary policy on employment, then the years prior to Burns added 6.4 percentage points to the inflation rate, whereas Burns added only 0.4 percentage points.

Labels: Burns, economics, macroeconomics, Mankiw

posted by knzn at 6/30/2006 12:18:00 PM

7 comments

![]()

![]()