Why did the stock market go up yesterday?

Barry Ritholtz, at The Big Picture, notes:

From the point of view of Mr. Market, the good news seems to be that the Fed is no longer likely to raise interest rates in August. I have a couple of problems with this good news. First, it may not even be true. Second, even if it is true, I don’t think it outweighs the bad news.

The inflation news was not good, by anyone’s estimation. One recognizes, of course, that the Fed is forward looking, and that the Fed would prefer, all other things being equal, to avoid a recession. The weak real GDP number might indicate a disinflationary slowdown, which might have a strong enough disinflationary impact to more than undo the observed increase in the inflation rate, which might lead the Fed to avoid tightening. But from the point of view of the Fed, might doesn’t necessarily make right. Right now the possibility of inflation getting out of control frightens the Fed more than does a recession. If recession is the cost of preventing an inflationary spiral, the Fed is willing to pay that cost.

Which brings me to the second point. If the Fed doesn’t tighten, it’s because the Fed thinks there is a serious risk of a recession. That can’t possibly be good news, can it?

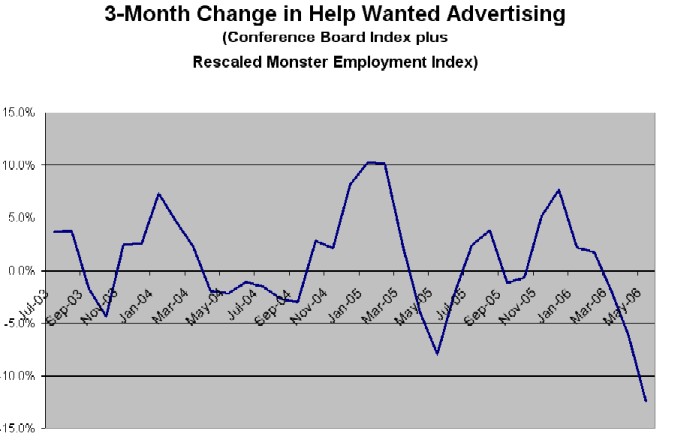

First, the bad news: The U.S. economy stunk the joint up in Q2, slowing sharply as inflation continued to climb.

The good news? You'll have to ask equity traders…

From the point of view of Mr. Market, the good news seems to be that the Fed is no longer likely to raise interest rates in August. I have a couple of problems with this good news. First, it may not even be true. Second, even if it is true, I don’t think it outweighs the bad news.

The inflation news was not good, by anyone’s estimation. One recognizes, of course, that the Fed is forward looking, and that the Fed would prefer, all other things being equal, to avoid a recession. The weak real GDP number might indicate a disinflationary slowdown, which might have a strong enough disinflationary impact to more than undo the observed increase in the inflation rate, which might lead the Fed to avoid tightening. But from the point of view of the Fed, might doesn’t necessarily make right. Right now the possibility of inflation getting out of control frightens the Fed more than does a recession. If recession is the cost of preventing an inflationary spiral, the Fed is willing to pay that cost.

Which brings me to the second point. If the Fed doesn’t tighten, it’s because the Fed thinks there is a serious risk of a recession. That can’t possibly be good news, can it?

Labels: capital, economics, finance, inflation, macroeconomics, profits, US economic outlook

posted by knzn at 7/29/2006 11:23:00 AM

7 comments

![]()

![]()

{kind=link}

{kind=link}